Did you know the average American saves less than 4% of their income? That means most of us are living right on the edge — one unexpected expense away from stress and struggle.

But there’s wisdom in an unusual place: the Bible points us to the ant.

“Ants are creatures of little strength, yet they store up their food in the summer.”

Proverbs 30:25

Ants aren’t strong, yet they’re called wise because they prepare ahead. They don’t wait until winter to think about food — they store it up in summer when it’s available. That’s exactly how saving works for us, too. It’s not about hoarding or being greedy. It’s about wisdom and preparation for the seasons we know are coming.

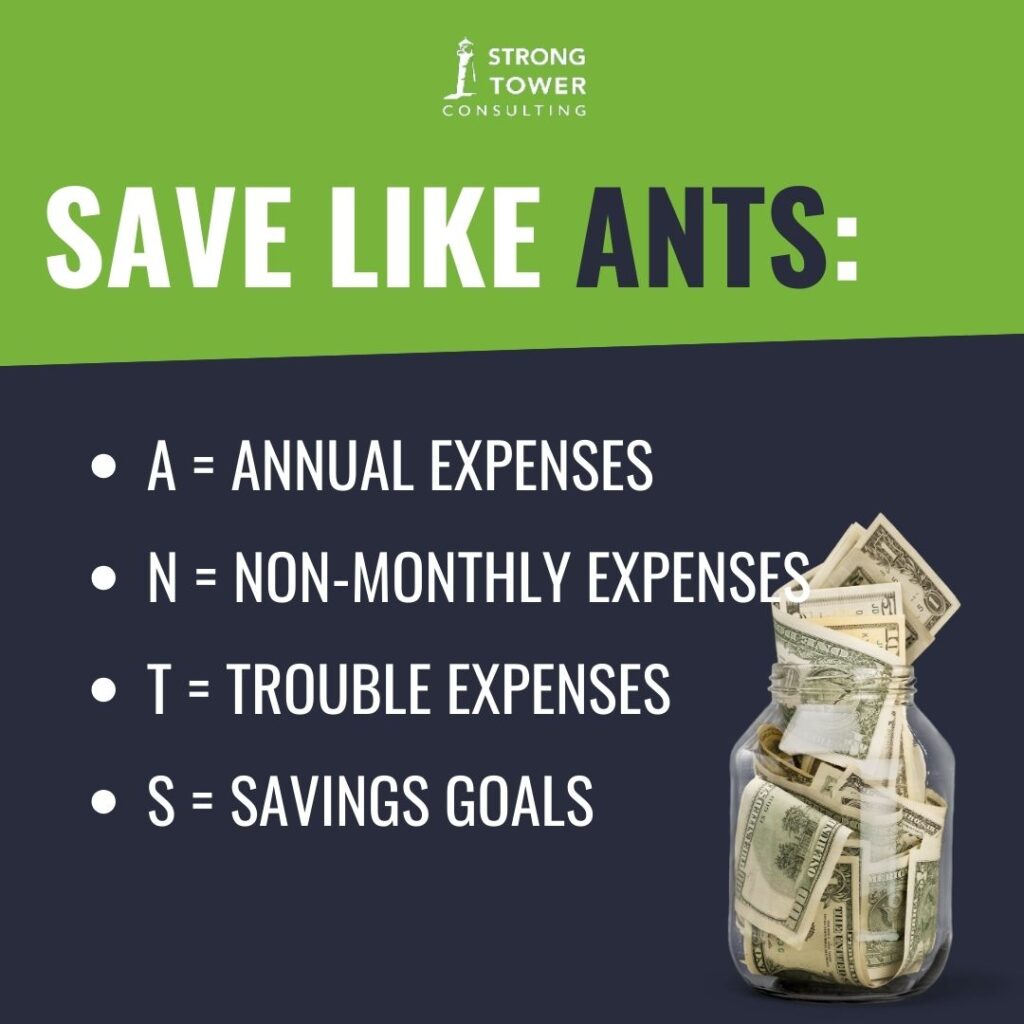

That’s why I like to teach people to save like ANTS:

- A = Annual Expenses

- N = Non-Monthly Expenses

- T = Trouble Expenses

- S = Savings Goals

Let’s break it down:

Save Like ANTS: A Simple Framework to Finally Build Consistent Savings

A = Annual Expenses

Think about it: why does Christmas always “sneak up on us”? Why do car registrations feel like a crisis every year? It’s not because we didn’t know they were coming. It’s because we didn’t prepare.

Here’s the fix:

- List every expense that happens once a year—Christmas, Amazon Prime, car registration, school tuition, property taxes.

- Add them up.

- Divide by 12.

That’s the amount you need to save each month.

👉 Example: If all your annual expenses total $1,200, divide by 12. That’s $100 per month. Set it aside automatically, and when Christmas rolls around, you’ll already have the cash.

Coach’s Tip: Put this money in a separate savings account labeled “Annual Expenses.” Out of sight, out of mind—and ready when you need it.

N = Non-Monthly Expenses

Non-monthly expenses are the budget busters. They’re not due every month, but they hit multiple times a year:

- Household repairs

- Kids’ sports and school activities

- Medical co-pays

- Clothing and shoes

Most families say, “We can pay our bills… until something extra comes up.” This is usually the problem—non-monthly expenses weren’t planned for. These funds are also called Sinking Funds and I explain more about them here if you want more information.

👉 The solution is the same as with annual expenses: estimate what you’ll spend for the year, add it up, and divide by 12.

If you know you’ll spend about $600 a year on car repairs, that’s $50/month. If sports fees run you $900 per year, that’s $75/month.

Coach’s Tip: Look back at your bank or credit card statements from last year to get realistic numbers. We tend to underestimate, but history doesn’t lie.

T = Trouble Expenses

These are the “when, not if” expenses:

- The water heater breaks.

- The car needs new brakes.

- The roof leaks during a storm.

A recent survey showed 56% of Americans can’t cover a $1,000 car repair without debt. That’s why building a trouble fund is non-negotiable.

Here’s how to approach it:

- Step 1: If you have debt, start with a $1,000 emergency fund. It’s not enough to cover everything, but it’s a critical buffer that keeps you from turning every hiccup into a credit card swipe.

- Step 2: Once you’re debt-free (except the house), build 3–6 months of living expenses. That’s your full emergency fund.

- Step 3: On top of that, set aside money for ongoing home and car maintenance. A good rule of thumb: about 1% of your home’s value per year.

👉 Example: If your house is worth $250,000, plan for $2,500/year in upkeep—new appliances, repairs, updates. That’s about $210/month.

Coach’s Tip: Trouble expenses aren’t glamorous, but they’re lifesavers. A flat tire won’t wreck your week when you’ve already got the cash ready.

S = Savings Goals

Finally—the fun part. Saving isn’t just about emergencies. It’s about your future, your dreams, and your why.

Short-term goals (3–6 months):

- Break the paycheck-to-paycheck cycle.

- Save your first $1,000.

- Pay off a small debt.

- Go one full month without overdraft fees.

Long-term goals (6 months–several years):

- Pay off all debt.

- Save for a house.

- Build retirement savings.

- Fund a legacy for your kids.

👉 Here’s the key: write them down. Studies show you’re 42% more likely to achieve goals when you write them down.

And don’t just write what—write why. Why does this matter to you? Your “why” will carry you through when you want to quit.

Coach’s Tip: Break big goals into checkpoints. Instead of staring at the mountain, aim for the next mile marker: the first $1,000 saved, the first credit card paid off. Each win builds momentum.

The Challenge for You

This week, start simple. Choose one category of savings to work on:

- List your annual expenses, total them up, and divide by 12.

- Or, tackle your non-monthly expenses and do the same.

Next month, add another category. Before long, you’ll have a full ANTS system in place—and for the first time, you’ll feel ahead instead of always scrambling to catch up.

Remember: ants aren’t strong, but they’re wise. And wisdom with money looks like preparing today for what you know is coming tomorrow.

Ready to Go Deeper?

Learning to save like ANTS is just the beginning. If you’re ready to build a financial plan that covers all the basics—from getting out of debt to creating a budget that works, to building lasting financial freedom—my book can guide you step by step.

📘 Level Up Your Finances: Say Goodbye to Winging It With Money will teach you how to:

- Save for annual, non-monthly, trouble expenses, and big goals.

- Break free from debt once and for all.

- Build confidence with money instead of stress.

- Create a path to true financial freedom.

Don’t just manage money—master it. Grab your copy today and start leveling up your finances!