You probably know your salary. You might even know your take-home pay. But do you know how much you actually make? Most people don’t… and it’s not because they’re bad with money. It’s because we’re taught to focus on the big number. The salary. The offer. The raise. But what you earn and what you keep are two very different things. That difference matters more than most people realize.

Let’s say you make $70,000 a year. On paper, that sounds great. But once you start peeling back the layers, you see a different story. Taxes come out first. Then health insurance. Maybe retirement contributions. Then there are the less obvious costs: gas to get to work, eating out because you’re tired, clothes for your job, little conveniences that make a busy life feel manageable. Before long, that $70,000 isn’t really $70,000 anymore.

How Much Do You Really Make? The Truth About Your Income

Why We Avoid the Numbers

If you’ve ever felt a little nervous to sit down and run your numbers, you’re not alone. In fact, a recent survey found that about 1 in 2 adults (52%) don’t know how much they spend each month. Income is one of the most commonly avoided questions in surveys as well. People either don’t know or hesitate to answer. There’s a reason for that. Looking closely at your finances can feel uncomfortable. But the unknown is almost always heavier than reality. It might be worse than you expected, or it might be better, but either way, knowing the truth gives you something solid to work with. That’s where peace starts.

Your Salary Isn’t the Full Story

We tend to focus on the big number, our annual salary, because it feels like the clearest measure of how we’re doing. But that number doesn’t tell the whole story. What you earn on paper and what you actually keep are two very different things. Once you begin to break it down, the gap between those numbers becomes impossible to ignore.

What Your W-2 Is Really Telling You

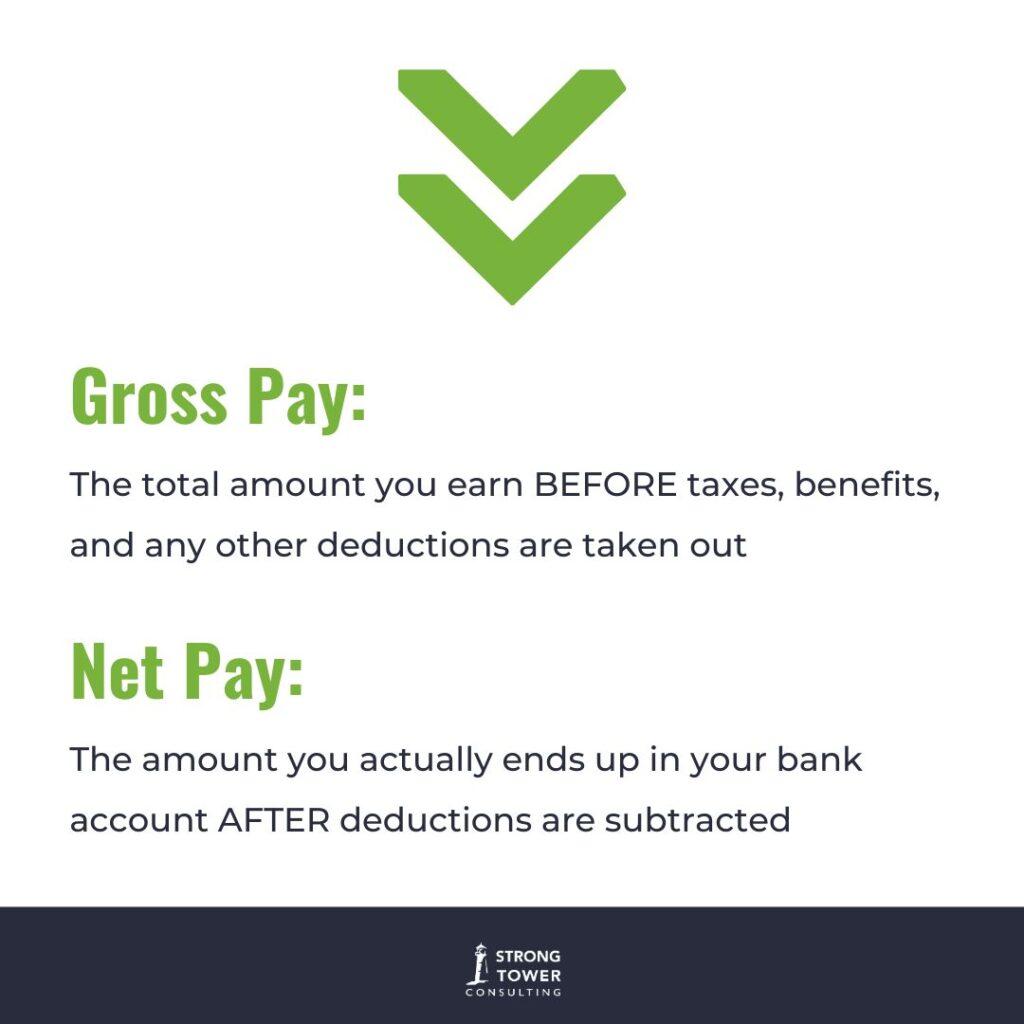

If you’ve ever looked at your paycheck and thought, Wait… where did it all go? A good place to start is with your W-2. It is easy to think of it as just another tax document, but it actually provides a clear snapshot of your income. Box 1 shows your taxable wages, which are often lower than your full salary, or gross pay, because contributions like retirement, health insurance, or other pre-tax benefits have already been deducted. Box 2 shows how much you paid in federal income taxes, while Boxes 4 and 6 reflect Social Security and Medicare taxes. State taxes are included as well, depending on where you live.

The amount that actually ends up in your bank account each month is your net pay, the money you can actually spend. Think of it this way: your gross pay is the flashy headline, and your net pay is the actual plot twist in the story of your paycheck. When you step back and look at the full picture, your W-2 reveals how much of your income never even made it to your wallet, a reality check that most people rarely take the time to see.

From Annual Numbers to Monthly Reality

From there, it’s important to connect that annual amount to your real, monthly life. Instead of estimating what you think you bring home, look at your actual bank deposits. What is consistently hitting your account each month? This step sounds simple, but it’s where clarity begins. Guessing creates stress. Real numbers create direction.

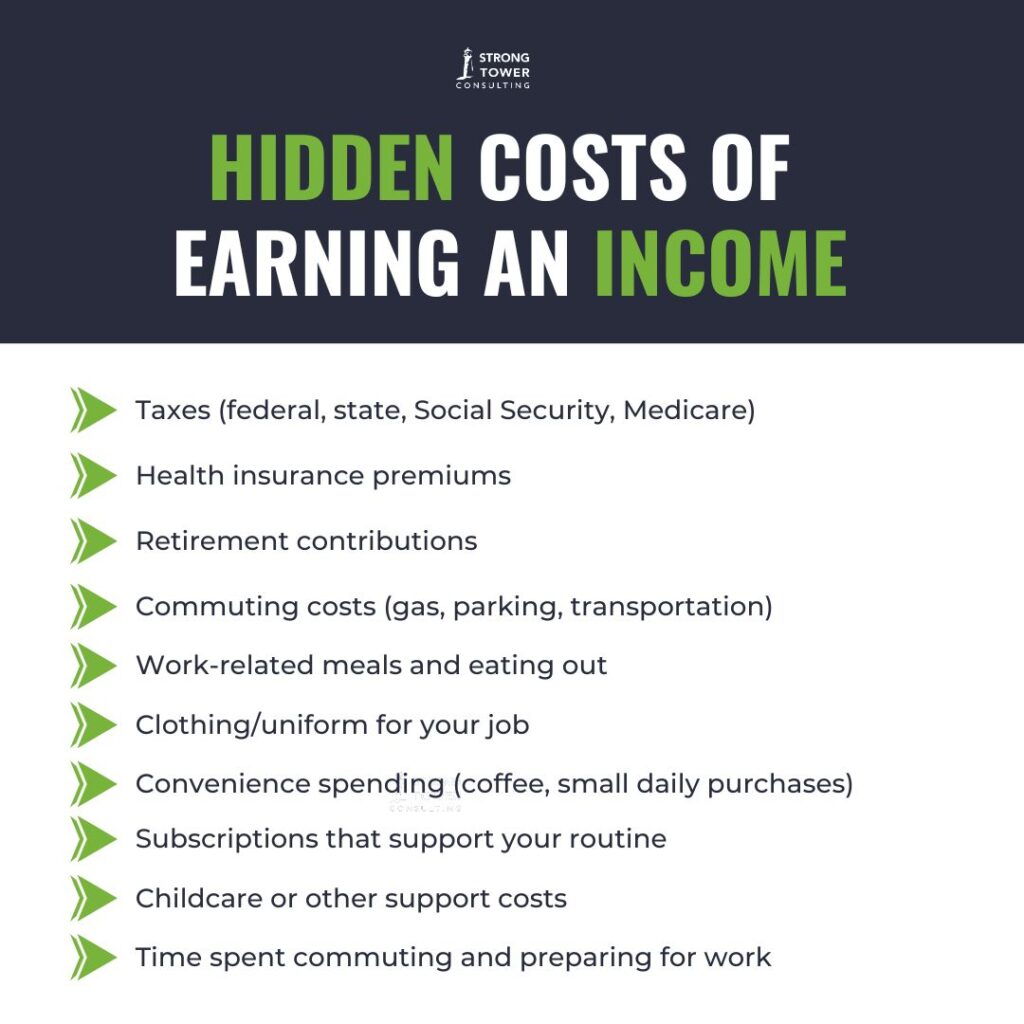

The Hidden Costs of Earning an Income

Even then, your take-home pay doesn’t tell the full story. There are everyday costs tied to earning and maintaining your income that often go unnoticed. Commuting, convenience spending, meals on busy days, subscriptions that make life easier – these are all small decisions that add up over time. And yes, the occasional latte counts… They may not feel directly connected to your income, but they shape how much of it you actually get to keep.

Your Time Matters More Than You Think

Time is another piece most people overlook. A 40-hour workweek rarely stays at 40 hours when you include getting ready, commuting, and decompressing at the end of the day. Your effective hourly rate might make you do a double-take… or cry into your coffee. Either reaction is valid. When you factor in the true number of hours your job requires, your effective hourly rate is often lower than you think. This isn’t meant to discourage you, but to give you a more accurate understanding of what your time is really worth. This also helps with keeping you grounded and not inflating your spending based on the gross that you make.

The Turning Point: Facing the Numbers

For many people, the hardest part of this process isn’t the math – it’s the moment of facing the numbers. This is where I see clients hesitate the most, and some are filled with a lot of anxiety about it. There’s often a fear that if they look too closely, they’ll confirm something they don’t want to see. But what consistently happens is this: once we walk through the numbers together, the tension lifts. Whether their situation is tighter than they hoped or better than they expected, they feel relief. Clarity replaces uncertainty, and that shift alone starts to create momentum.

Where Financial Freedom Actually Begins

The goal isn’t just to make more money. It’s to understand it, to manage it with intention, and to make sure it’s supporting the life you actually want. Financial freedom doesn’t begin with a raise or a perfect budget. It begins with awareness.

Turning on the lights in your financial life starts with something simple but powerful: knowing how much you actually make each month. Not what you assume, not what you hope—what’s real. From there, every decision becomes clearer, and every step forward becomes more grounded in truth.

How to Figure Out What You Really Make

1. Start with your W-2.

Look at Box 1 for your taxable income and note how it compares to your full salary. Then review Boxes 2, 4, and 6 to see how much went to taxes. This gives you a big-picture view of where your money is going before it even reaches you.

2. Calculate your true monthly income.

Open your bank account and look at what was actually deposited over the last 2–3 months. Find the average. This is your real monthly income, not an estimate.

3. Compare expectation vs. reality.

Write down what you thought you made per month, then compare it to your actual number. This gap is where awareness begins.

4. Identify work-related spending.

List out expenses that are directly or indirectly tied to your job: gas, eating out, convenience purchases, subscriptions. These reduce what you truly keep.

5. Do a simple “keep” calculation.

Take your real monthly income and subtract those work-related costs. What’s left is closer to what you actually have available to build your life.

6. Reflect before you react.

Don’t rush to fix everything at once. Just sit with the numbers. Clarity comes first. Better decisions come next.

Level Up Your Finances

Once you know your actual take-home pay, you can start to level up your finances in a real way. This means creating a budget based on the money that actually lands in your account, not what you think you make or wish you had. Each paycheck can then be intentionally allocated to cover your essential expenses, savings goals, and discretionary spending, giving you control instead of guessing or reacting. This approach makes your money work for you rather than the other way around, and it sets the foundation for smarter financial decisions every month. For more guidance, you can explore other budgeting resources and tools that make this process easier.

Awareness Leads to Clarity

Understanding how much you really make is the first step toward financial freedom. Once you have clarity, you can make intentional choices, build a budget that works for your life, and start seeing real results. If you want a complete guide to taking control of your money, my book Level Up Your Finances walks you through the process step by step. And if you want more personalized support, my coaching services provide hands-on help to make sure you’re not just learning, but actually applying strategies that help you save, plan, and feel confident about your financial future.